Learn about the City’s local boards and shared service agencies in the budget manual

Local boards and shared services

There are seven local boards and shared services (LBSS) that the City funds in whole or in part. These agencies have separate governance structures and maintain varied types of relationships with the City. More information about the City’s LBSS is available in the budget manual.

For 2026 budget confirmation, the budget confirmation process continues to be separated into two phases: City budget confirmation and LBSS agencies budget confirmation.

The LBSS budget process is not impacted by the Strong Mayor timeline, as the budget preparation and submission processes are defined in the governing statutes applicable to each LBSS organization. The power of Council to amend and/or approve the budget of each local board or shared services provider also varies based on the governing legislation, as summarized in report 2026-29 Budget Confirmation Local Boards and Shared Services Agencies.

This year, the Mayor respectfully requested LBSS agencies to join the City in finding ways to limit budget increases for 2026.

Tax-supported LBSS budget confirmation

Similar to the presentation of City services budget information, Table 63summarizes the respective contribution to the total tax levy requirement, net of their proportionate allocation of assessment growth, of the City’s LBSS agencies 2026 confirmed budget.

Table 63 LBSS 2026 confirmed budget update impact on tax levy net of allocated assessment growth

| LBSS agency | 2025 Confirmed Budget $ | 2026 Forecast Increase (net of assessment growth) $ | 2026 Confirmed Increase (net of assessment growth) $ | Change from 2026 Forecast to 2026 Confirmed | 2026 change over 2025 % | 2026 Confirmed tax levy impact (net of assessment growth) % |

|---|---|---|---|---|---|---|

| Guelph Police Services | 67,222,764 | 3,809,518 | 5,793,836 | 1,984,318 | 9.9% | 1.65% |

| County of Wellington | 33,730,669 | 3,942,304 | 7,747,099 | 3,804,795 | 24.3% | 2.21% |

| Guelph Public Library | 12,349,767 | 1,735,761 | 1,813,241 | 77,480 | 16.0% | 0.52% |

| Wellington-Dufferin-Guelph Public Health | 4,569,795 | 43,381 | 78,142 | 34,761 | 2.9% | 0.02% |

| The Elliott Community | 2,944,546 | 30,910 | 26,241 | (4,668) | 2.1% | 0.01% |

| Total LBSS agencies’ tax impact | 120,817,541 | 9,561,873 | 15,458,560 | 5,896,686 | 14.07% | 4.40% |

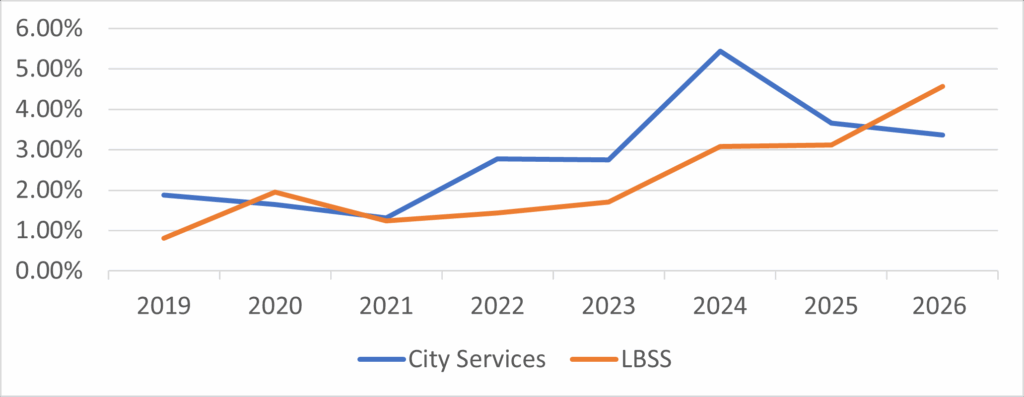

Historically, slightly more than two‑thirds of Guelph’s property tax levy has supported City services and slightly less than one‑third has supported the LBSS agencies. In recent years, this balance has shifted as LBSS tax-supported budgets have grown at a faster rate than the City’s tax-supported budget. Rising cost pressures and increasing service demands for several LBSS agencies have required higher annual increases than in the past. The growth of the tax-supported budget over time is shown in Figure 9.

Figure 9: tax increase over time

View Figure 9 data

| Year | City Services | LBSS |

| 2019 | 1.88% | 0.81% |

| 2020 | 1.65% | 1.95% |

| 2021 | 1.31% | 1.24% |

| 2022 | 2.78% | 1.43% |

| 2023 | 2.75% | 1.71% |

| 2024 | 5.44% | 3.08% |

| 2025 | 3.66% | 3.12% |

| 2026 | 3.36% | 4.40% |

*City Services figure excludes the Hospital Levy of 0.11%

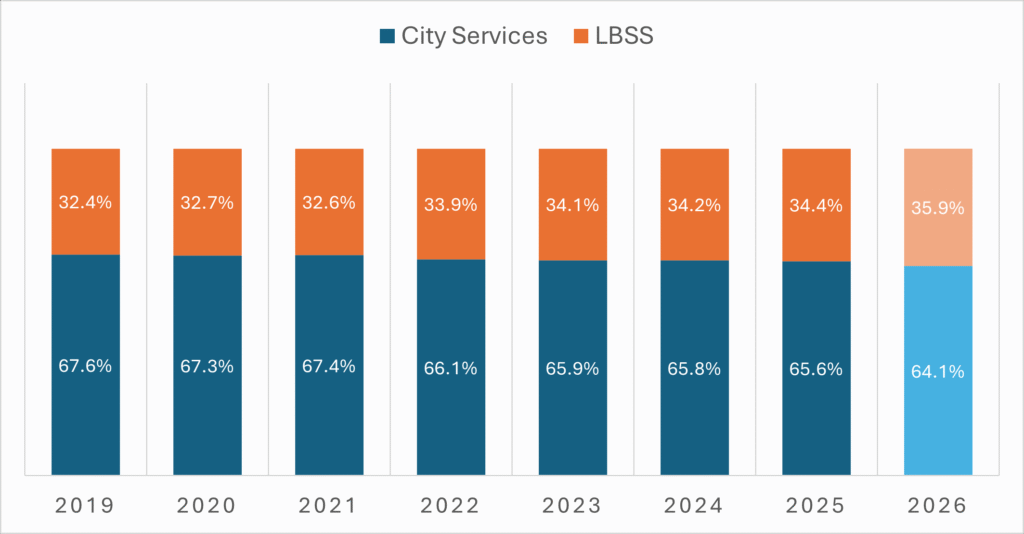

Over the past several years, Guelph, like many communities, has experienced increased pressures related to supporting community members at risk of or experiencing homelessness, mental health, and substance use disorder. At the same time, as we have heard in previous budget presentations, police services across the province have been challenged to address significant increases in online luring, intimate partner violence, and human trafficking. Responding to these challenges has put pressure on the City’s budget in multiple ways, including increased costs for services and financial support delivered directly by the City (e.g., by-law response, Welcoming Streets, paramedic services, daytime space, and more). It has also driven significant increases in some local board budgets, at an order of magnitude great enough to drive a shift in the overall composition of how property tax funding is allocated between City services and LBSS, as presented below in Figure 10.

Figure 10: Allocation of tax-supported funds between city services and LBSS

View Figure 10 data

| Year | City Services | LBSS |

| 2019 | 67.60% | 32.40% |

| 2020 | 67.30% | 32.70% |

| 2021 | 67.40% | 32.60% |

| 2022 | 66.10% | 33.90% |

| 2023 | 65.90% | 34.10% |

| 2024 | 65.80% | 34.20% |

| 2025 | 65.60% | 34.40% |

| 2026 | 64.06% | 35.94% |

Although the change may not appear dramatic at first glance, the shift over time has been significant. In 2019, prior to the COVID‑19 pandemic, 67.7% of property tax revenue supported City services, while 32.3% was allocated to LBSS. By 2026, this distribution is projected to shift to 64.06% for City services and 35.94% for LBSS (Table 64):

| Budget | 2019 (pre-covid) | 2026 Confirmed | Change |

|---|---|---|---|

| City Services | 67.7% of tax levy | 64.1% of tax levy | (3.6%) |

| LBSS | 32.3% of tax levy | 35.9% of tax levy | 3.6% |

Digging further into these changes at the local board level, the major drivers of this shift are from increased costs to deliver social services and policing for our community (Table 65):

| Local Board | 2019 (pre-covid) | 2026 Confirmed | Change |

|---|---|---|---|

| Guelph Police Services | 17.2% | 19.3% | 2.1% |

| County of Wellington | 9.1% | 10.9% | 1.8% |

| Guelph Public Library | 3.8% | 3.7% | (0.1%) |

| Wellington-Dufferin-Guelph Public Health | 1.6% | 1.2% | (0.4%) |

| The Elliott Community | 0.6% | 0.8% | 0.2% |

| Total | 32.3% | 35.9% | 3.6% |

City contingency reserves were also utilized to phase-in a significant increase in social services costs in 2024, with phase-in offsets of $4.2 million in 2024, $2.8 million in 2025, and $1.4 million in 2026. In 2027, the City will fully budget for the social services costs in alignment with the County’s budget for the City share of the costs.

Information about the 2026 tax-supported LBSS agencies budget updates can be found within their respective budget materials linked below.

Guelph Police Services

- GPS Board meeting video, October 23, 2025

- 2026 Budget Confirmation, October 23, 2025

- GPS Board meeting video, January 12, 2026

- 2026 Special Budget Meeting, January 12, 2026

County of Wellington

- 2026 Budget Report: Social Services, January 29, 2026

- Historically, the City has under budgeted for Social Services due to actual year-end surplus trends. However, in 2023, this surplus trend reversed, and there was a significant budget increase for 2024 to respond to housing and homelessness challenges in our community. In the 2024-2027 Multi-Year Budget (MYB), the City phased in the increase over the four-year period. The 2024 budget adopted by Council included a phase-in offset of $4.2 million for 2024, and a plan to decrease the phase-in by $1.4 million each year in 2025, 2026, and 2027. Table 66 provides a reconciliation from the County’s budget increase for the City’s social services costs and the City’s budgeted increase including the impact of the phase-in. The City’s 2026 budget continues to include a phase-in of the tax levy impact through reserve transfers totaling $1.4 million from the Tax Operating Contingency Reserve (#180).

Table 66 County/City Budget Reconciliation (in $ millions)

| County budget increase per January 14, 2026 draft budget approved by Joint Social Services and Land Ambulance Committee for recommendation to County Council | 6.8 |

| 2024 budget phase-in impact | 1.4 |

| Allocated assessment growth revenue | (0.4) |

| City net tax levy increase for Social Services per Table 50 | 7.7 |

*Total may not add due to rounding

Guelph Public Library

- Guelph Public Library Board approved budget totaling $14,923,874 in October 2025.

- Guelph Public Library Board met on January 26, 2026 to review budget amendments to the previously approved 2026 budget update. The Board approved a 2026 operating budget of $14,329,053, reflecting a decrease of $594,821 from the amount previously approved in October.

Wellington-Dufferin Guelph Public Health

- Wellington-Dufferin Guelph Public Health Draft Budget, October 1, 2025.

The Elliott Community

- The Elliott Community 2026 Budget.

Downtown Guelph Business Association

The Downtown Guelph Business Association (DGBA) budget is also included for Council approval. This is a special levy that is applied to downtown commercial properties in addition to the City’s general taxation requirement. Table 67 summarizes the 2026 confirmed budget for the DGBA.

Table 67 DGBA 2026 confirmed budget

| DGBA confirmed budget | 2026 adopted budget $ | 2026 confirmed budget $ | Change from 2026 adopted to confirmed $ |

|---|---|---|---|

| Gross expense budget | 742,836 | 807,754 | 64,918 |

| Total levy requirement | 742,836 | 742,836 | 0 |

Non-tax-supported LBSS budget confirmation

The City’s share of the Grand River Conservation Authority (GRCA) budget is funded through the Water and Wastewater Services user rates. The 2026 confirmed GRCA budget has not changed from adopted, Table 68.

Table 68 GRCA 2026 confirmed budget

| GRCA confirmed budget | 2025 adopted budget | 2026 forecast increase | 2026 confirmed increase | Change from 2026 forecast to confirmed |

|---|---|---|---|---|

| Gross expense budget ($) | 1,863,400 | 50,000 | 50,000 | 0 |

| Total rate impact (%) | n/a | 0.00% | 0.00% | 0.00% |

*The draft 2026 budget submission from GRCA is $1,888,900, a year over year increase of $25,500. Given the draft status of the GRCA budget, that the difference between the adopted budget and the update falls into the administrative change category under the City’s Budget Policy, and this difference does change the utility rates, it has not been updated in 2026.

LBSS capital budget confirmation

The Program of Work for Other Boards and Agencies includes capital projects that belong to GPS and GPL. The 2026 capital budget for this Program of Work has decreased by $500,000 from the 2026 forecast due to the removal of the GPL project for virtual desktop infrastructure. Details of the budgeted investments can be found within their respective budget materials, linked above. The capital budgets of both organizations are funded through transfers from capital reserve funds, and the transfers to the capital reserve funds are reflected in the operating budgets for both organizations, therefore, these capital budgets do not represent an additional tax levy impact.

LBSS reserve and reserve fund confirmation

GPS and GPL both have contingency and capital reserve funds that under the City of Guelph General Reserve and Reserve Funds policy, require Council approval of transfers that are embedded within the operating and capital budgets of GPS and GPL, and they are therefore presented here in Table 69 through 75.

Table 69 Library Contingency reserve (102) budget and forecast ($ millions)

| Description | 2025 | 2026 | 2027 | 2028 | 2029 |

|---|---|---|---|---|---|

| Opening balance | 0.22 | 0.22 | 0.22 | 0.22 | 0.22 |

| Total revenue | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Total expenditures | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Closing balance | 0.22 | 0.22 | 0.22 | 0.22 | 0.22 |

Table 70 Library Capital reserve fund (157) Forecast ($ millions)

| Description | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Opening balance | 1.65 | 1.31 | 1.45 | 1.58 | 1.45 | 1.48 | 1.26 | 1.38 | 1.62 | 1.72 | 1.78 |

| Total revenue | 0.33 | 0.34 | 0.35 | 0.36 | 0.38 | 0.39 | 0.40 | 0.41 | 0.42 | 0.44 | 0.45 |

| Total expenditures | (0.68) | (0.20) | (0.22) | (0.50) | (0.35) | (0.61) | (0.28) | (0.18) | (0.32) | (0.38) | (0.34) |

| Closing balance | 1.31 | 1.45 | 1.58 | 1.45 | 1.48 | 1.26 | 1.38 | 1.62 | 1.72 | 1.78 | 1.89 |

Table 71 Library Development Charge reserve fund (316) Forecast ($ millions)

| Description | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Opening balance | 6.79 | (10.86) | (10.30) | (9.45) | (7.96) | (6.39) | (4.74) | (3.67) | (2.55) | (1.40) | (0.24) |

| Total revenue | 0.56 | 0.78 | 0.96 | 1.59 | 1.64 | 1.69 | 1.09 | 1.12 | 1.15 | 1.16 | 1.20 |

| Total expenditures | (18.21) | (0.23) | (0.11) | (0.09) | (0.07) | (0.04) | (0.01) | – | – | – | – |

| Closing balance | (10.86) | (10.30) | (9.45) | (7.96) | (6.39) | (4.74) | (3.67) | (2.55) | (1.40) | (0.24) | (0.96) |

| Balance including outstanding debt | (3.73) | (4.32) | (4.62) | (4.30) | (3.92) | (3.50) | (3.67) | (2.55) | (1.40) | (0.24) | (0.96) |

Table 72 Police Contingency reserve (115) budget and forecast ($ millions)

| Description | 2025 | 2026 | 2027 | 2028 | 2029 |

|---|---|---|---|---|---|

| Opening balance | 2.73 | 2.45 | 2.21 | 2.21 | 2.21 |

| Total revenue | (0.28) | – | – | – | – |

| Total Expenditure | – | (0.24) | – | – | – |

| Closing balance | 2.45 | 2.21 | 2.21 | 2.21 | 2.21 |

Table 73 Accumulated Sick Leave (Police) reserve (101) budget and forecast ($ millions)

| Description | 2025 | 2026 | 2027 | 2028 | 2029 |

|---|---|---|---|---|---|

| Opening balance | 5.05 | 4.65 | 4.25 | 3.85 | 3.45 |

| Total revenue | – | – | – | – | – |

| Total Expenditure | (0.40) | (0.40) | (0.40) | (0.40) | (0.40) |

| Closing balance | 4.65 | 4.25 | 3.85 | 3.45 | 3.05 |

Table 74 Police Capital reserve fund (158) Forecast ($ millions)

| Description | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Opening balance | 5.14 | 3.14 | 2.93 | 1.09 | 0.82 | 1.34 | 0.77 | 2.08 | 2.71 | 0.95 | 6.54 |

| Total revenue | 4.44 | 5.18 | 5.36 | 5.51 | 5.66 | 5.82 | 5.98 | 6.15 | 6.32 | 6.50 | 6.69 |

| Total expenditures | (6.44) | (5.39) | (7.20) | (5.78) | (5.14) | (6.39) | (4.67) | (5.52) | (8.08) | (0.92) | (0.92) |

| Closing balance | 3.14 | 2.93 | 1.09 | 0.82 | 1.34 | 0.77 | 2.08 | 2.71 | 0.95 | 6.54 | 12.31 |

Table 75 Police Development Charge reserve fund (324) Forecast ($ millions)

| Description | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Opening balance | (16.91) | (19.39) | (18.97) | (18.41) | (17.04) | (15.61) | (14.11) | (13.12) | (12.09) | (10.99) | (9.71) |

| Total revenue | 0.67 | 0.94 | 1.17 | 1.97 | 2.03 | 2.09 | 1.56 | 1.61 | 1.66 | 1.51 | 1.56 |

| Total expenditures | (3.16) | (0.51) | (0.61) | (0.60) | (0.60) | (0.59) | (0.58) | (0.57) | (0.56) | (0.23) | (0.21) |

| Closing balance | (19.39) | (18.97) | (18.41) | (17.04) | (15.61) | (14.11) | (13.12) | (12.09) | (10.99) | (9.71) | (8.36) |

| Balance including outstanding debt | (8.91) | (9.23) | (9.15) | (8.27) | (7.34) | (6.36) | (5.92) | (5.44) | (4.92) | (4.23) | (3.50) |

LBSS confirmed assessment growth revenue

Budgeted assessment growth revenue of $1.33 million was allocated to offset the LBSS tax levy impact, based on estimated assessment growth of 1.15 per cent. Actual assessment growth returned for 2025 was 1.34 per cent, and the additional assessment growth revenue of $204 thousand was applied to reduce the 2026 tax levy impact, contrary to the prescribed treatment under Revenue Budgeting Policy. A recommendation for Council approval of this policy deviation is included in the staff report.

| 2026 Confirmed Budget |

|---|

| Council reports |

| Budget board |

Related pages

City budget

Previous annual budgets

Budget manual

Budget Policy

Watch and listen

Mayoral direction

Mayoral direction response from staff

Mayoral decision – Budget Amendment

Printable 2026 Budget update

Printable 2026 Budget Update – LBSS

Latest updates

Timeline

October 16: Mayor Cam Guthrie’s draft 2026 Budget Update Released

October 29: Special Council – 2026 Budget Update

November 18: Special Council – 2026 Budget public delegations

November 26: Special Council – 2026 Budget amendments

December 17: Special Council – 2026 Budget local boards and shared services